Bubble Watch: Canadian Housing (Guest Article)

This week’s piece is a guest article on a potential housing bubble in Canada from Greg Levin. Greg runs a fantastic newsletter of his own called BubbleCatcher. In his own words, Greg’s newsletter is a “realistic and fact-based analysis of the economy and global geopolitical space. No hidden agendas. No talking one’s book. Just our take on the facts.“ For more of his great content, you can check out Greg’s newsletter here.

If you’re an American looking to buy a home, life kind of sucks right now. But you know where life sucks even more?

Canada.

That’s right. Syrup-drinkin’, hockey-luvin’ Canada. Where first-time homebuyers are living in a horror show.

Canadian is seeing an eye-watering increase in housing prices that puts even America to shame.

After the financial crisis of ‘08, the Canadian housing market raced ahead of the U.S. at a blistering speed. The acceleration has been so fast that the Bank of Canada recently reported it as a risk to the financial system:

“Many Canadians are spending more of their work and leisure hours at home and they are looking for larger places to live. But the number of houses available to buy is limited, and prices in several housing markets are rising quickly. What’s more, some people may be buying homes now because they expect prices to keep climbing, and this is a concern. If house prices and household incomes were to fall in the future because of a shock to the economy, some households could need to cut back on spending. This would slow the economy and possibly put stress on the financial system.” - Bank of Canada Financial System Review [link]

Let’s read that again:

“… some people may be buying homes now because they expect prices to keep climbing [emphasis added].”

This is one of several key indicators of a bubble: overly optimistic behavior that feeds on itself and sparks a fear-of-missing-out / manic-like buying.

The IMF had also noted its concerns back in a report in 2019. Note that at that time, housing prices had cooled down a bit as authorities had just tightened monetary policy. But the report noted prices in major markets like Toronto, Hamilton, and Vancouver were still “overvalued”. Now that monetary policy has been loosened again due to covid, froth has returned in full force.

But remember, irrational optimism is only one ingredient of a bubble. The other is excess leverage.

Are we seeing excess leverage? Yes.

Canada has had rock bottom interest rates over the last few years, giving huge incentives for taking on leverage. This isn’t big news, and it’s essentially the same in most places in the world now.

There are generally fewer capital gains taxes on residential property in Canada. Capital gains taxes on one’s principal residence are waived in Canada. In the U.S., they are waived only if you meet certain requirements. When comparing the two, this could incentivize people to push a heavier allocation into real estate versus stocks.

Canadians take on more debt than Americans. Mortgage debt growth in Canada has outpaced the U.S. starting in 2010. This pace continues even in the wake of covid. Why this is happening seems to be unknown. This report by BMO Economics suggests that perhaps Canadians may have simply collectively “chosen” to consumer more housing resources than the U.S. I think it has more to do with supply-side factors (see below).

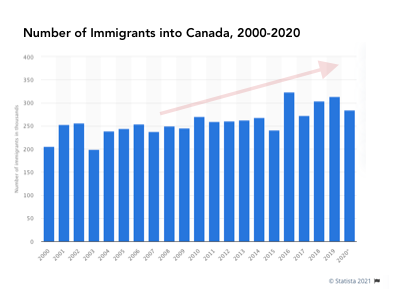

Longer-term, Canada has steadily increased its immigrant numbers. Roughly 21.5 percent of the population is an immigrant with permanent residence. And for good reason: Canada has been rated one of the best countries for welcoming immigrants. Many of the countries these immigrants come from are experiencing high growth themselves, such as China, India and the Philippines, giving them more buying power. However, researchers have proven that while immigration may be playing a role in housing prices, the net effect is small.

Housing supply has also been a major factor:

Covid has disrupted supply chains, making key commodities like steel, copper, and lumber extremely expensive. Again, we’ve highlighted this before for the U.S. But even after months of getting supply chains online again, we still see prices elevated.

Canada is a more heavily regulated / heavily zoned market than the U.S. This adds costs to the price of a home. This was made clear in a paper by Edward Glaeser and Joseph Gyourko, which details the extra wealth that is generated from these costs gets passed onto the sellers, i.e. the individuals who already owned homes before building constraints were imposed. And because these rules are determined by existing homeowners, new development projects become progressively harder to build.

So what does this mean going forward? Here’s a forecast:

Upward pressures on housing prices are likely to remain for the short term. Housing prices today seem to be higher due to a mix of both supply constraints (government policies) and demand factors (cheap credit, new demand, investing preferences). Because some of these factors are structural in nature, it may take a while for prices to cool.

Ultimately, pressures may subside as affordability maxes out. Homebuyers will inevitably hit constraints due to being overleveraged.If this ends in a healthy manner, we could see price pressures fade as the next cyclical slowdown in the economy rolls through. The post-covid mania will inevitably fade, although the exact timing of this all is hard to predict.

Key risk factor: look for signs of mania-induced leverage. We already see signs of manic-type behavior in buyers: bidding wars, call cash offers, huge lines for open houses, etc. This is happening in the U.S., too, but the runup in prices isn’t as severe here and aggregate household debt levels are more manageable. Canadian bank regulators will need to remain extra vigilant and prevent excessive leverage from being taken on by homebuyers.

External shocks could put the mortgage industry in trouble and spread to the broader economy. When bubbles occur, people take on undue risks because people get greedy. Bankers see their hedge fund neighbors buying a new Tesla and want one too. So they dream up new products to sell to the public. When the economy inevitably turns, the problems of overleverage come to the fore, and mortgage insurers would be the most at risk. Banks that are heavily invested in the mortgage space, such as the Royal Bank of Canada, will also be vulnerable. Keep an eye out.

*special thanks to BS for helping me with this report

References:

Kindleberger, C. (1978). Manias, Panics, and Crashes: A History of Financial Crises. Basic Books.

Jones, B. (2014). "Identifying Speculative Bubbles; A Two-Pillar Surveillance Framework." IMF Working Papers, International Monetary Fund.

Disclaimer: BubbleCatcher is published as an information service for subscribers, and it includes opinions as to forecasts on the global economy and its impact on securities linked to economic activity. The publishers of BubbleCatcher are not brokers or investment advisers, and they do not provide investment advice or recommendations directed to any particular subscriber or in view of the particular circumstances of any particular person. BubbleCatcher does NOT receive compensation from any of the companies featured in our articles. At various times, the publisher of BubbleCatcher may own, buy or sell the securities discussed for purposes of investment or trading. BubbleCatcher and its publishers, owners and agents, are not liable for any losses or damages, monetary or otherwise, that result from the content of BubbleCatcher. Past results are not necessarily indicative of future performance. The information contained on BubbleCatcher is provided for general informational purposes, as a convenience to the subscribers of BubbleCatcher. The materials are not a substitute for obtaining professional advice from a qualified person, firm or corporation. Consult the appropriate professional advisor for more complete and current information. BubbleCatcher makes no representations or warranties about the accuracy or completeness of the information contained on this website. Any links provided to other server sites are offered as a matter of convenience and in no way are meant to imply that BubbleCatcher endorses, sponsors, promotes or is affiliated with the owners of or participants in those sites, or endorses any information contained on those sites, unless expressly stated.